When Your Moat Becomes a Trap: What Nearly Two Decades in Building Products Taught Me About the Advantages that Quietly Become Liabilities

Every building product company I’ve worked for and with wanted the same thing. A moat. Something customers couldn’t leave, suppliers couldn’t squeeze, and competitors couldn’t copy.

I’ve watched building product companies build their moats. I’ve helped build a few myself. And I’ve watched them turn on us.

But here’s what I learned the hard way:

The same competitive advantages that protect you from rivals today can chain you to dying technologies, evaporating supply chains, and hostile customers tomorrow.

I’ve watched it happen. As a VP leading multi-million dollar product launches in the building materials space, I’ve seen companies with “impenetrable” advantages get disrupted not despite their moats, but because of them.

Let’s talk about what real moats look like in building products and Contech, and more importantly, how to build defenses without building your own prison.

Table of Contents

The Classic Moats: What Product Leaders Think They Want

As product leaders we love citing the tech industry playbook on moats, with their network effects, economies of scale and switching costs. We’d have customer lock-in through workflow integration and first mover/disruptor status in emerging categories.

The tech playbook works in industries that can pivot in sprints. But in the construction industry we pivot in decades.

Code listings take years.

Spec-sheet credibility takes years.

Relationships take careers.

The ConTech Cautionary Tale: When “Sticky” Becomes “Stuck”

Let me start with the software side, because the lessons are clearest there.

When Lock-In Backfires

One of the dominant Contech platforms built an empire on stickiness: deep workflow integration, years of project data, trained teams, astronomical switching costs.

And a growing segment of its users started looking for the exits.

Why? The complaints are remarkably consistent.

Pricing Structure: Some platforms charge based on total construction volume — typically 0.1–0.2% of project cost. A $20M job? That’s $20K–$40K in annual fees. Regardless of whether you’re using the features. Regardless of project activity.

Forced Bundling: Teams pay for modules they don’t need because everything’s packaged together. Small contractors end up with six-figure contracts for tools they barely touch.

Friction with Design Tools: Want to connect your BIM models, RFIs, and field data? Get ready for third-party workarounds, manual data transfers, and expensive custom integrations.

The moat worked. The incumbent dominated. But now the market is shopping — and the alternatives are multiplying.

The Autodesk Evolution

Autodesk’s story is different but equally instructive. AutoCAD and Revit have what one industry analyst called “insane switching costs”—they’re undeniably industry standards.

But Autodesk recognized something critical: dominance in design software didn’t automatically translate to dominance in project management.

Instead of building a moat through lock-in, they built bridges. Native connections to AutoCAD, Revit, and Navisworks. Modular licensing where you pay for what you use. An open ecosystem of pre-built integrations.

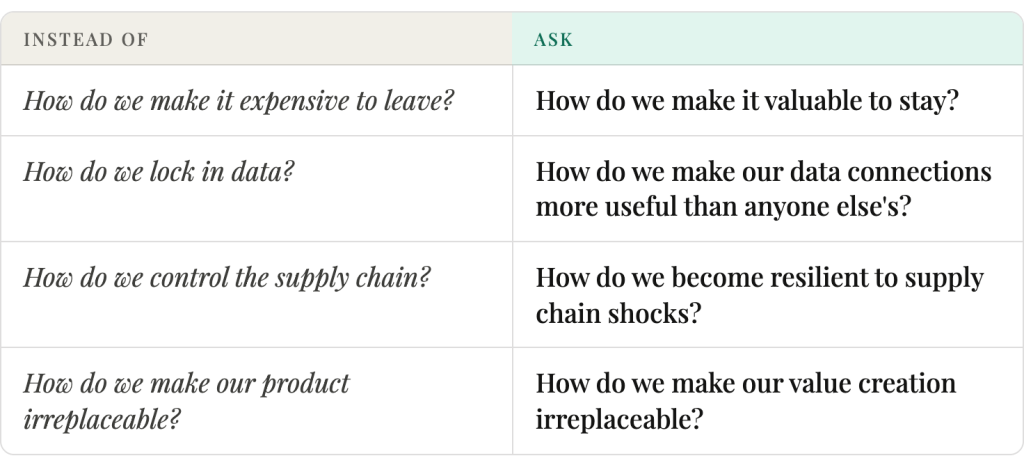

The best moat isn’t making it impossible to leave. It’s making it impossible to want to.

The Emerging Alternative: SubmittalLink’s Strategy

But here’s where it gets interesting. While the giants fight over enterprise accounts, a new category of solutions is winning by going narrower and cheaper.

SubmittalLink charges $150/month with unlimited projects and users. All features included. No upsells. No hidden fees.

They’re not trying to be everything to everyone. They focus on submittals, RFIs, drawings, and punch lists—the fundamentals that teams actually use every day.

Their positioning? “We were paying a fortune for other software but only using a small portion of it.”

This is the Profit Arc principle applied to software: Know what your customers actually value, strip out everything else, and price accordingly.

The takeaway for building product manufacturers: Your moat only works if customers feel they’re getting proportional value. Otherwise, you’re just creating the conditions for your own disruption.

Building Materials: When Your Supply Chain Becomes a Single Point of Failure

Now let’s talk about physical products, where the stakes are even higher.

James Hardie: The Fiber Cement King’s Careful Balance

James Hardie dominates fiber cement with roughly 90% market share in North America. They pioneered the technology in the 1980s after recognizing asbestos was unsustainable.

Their moats are textbook:

- Manufacturing Scale: $100M+ invested in R&D, five generations ahead of generic fiber cement

- Brand Equity: The #1 siding brand, trusted on 10M+ homes

- Proprietary Technology: Engineered for Climate® products with specific formulations for regional conditions

- Distribution Lock-in: Multi-year exclusivity agreements with top homebuilders (Meritage Homes, David Weekley)

But here’s what’s interesting: James Hardie understands that moats require continuous investment.

They’re not sitting still. Their $8.75B acquisition of AZEK (closed late 2025) expands their addressable market by 50% and adds $625M in synergies. Their Low Carbon Cement Technology Roadmap targets 50% CO₂ reduction by 2030.

The Hardie Operating System (HOS)—their lean manufacturing framework—delivered a 27.8% adjusted EBITDA margin even while pulp and cement costs surged.

This is the critical difference: James Hardie’s moats aren’t static defenses. They’re dynamic capabilities that require constant reinvestment.

The Fiber Cement Vulnerability: Raw Materials

But even James Hardie isn’t immune to supply chain risk. Fiber cement requires specific raw materials:

- Portland cement (price-sensitive to energy costs)

- Cellulose fibers from wood pulp (subject to forestry regulations and availability)

- Silica sand (geographically concentrated)

- Fly ash

- Water (increasingly regulated)

Fly ash (a byproduct of coal power plants) used to be abundant and cheap for fiber cement production. But as coal plants shut down for environmental reasons, fly ash availability is declining.

This is the double-edged sword of raw material moats: The specialized inputs that prevent competitors from easily replicating your product also create dependencies you don’t control.

James Hardie’s response? They’re investing in synthetic gypsum (33% of U.S. gypsum supply) and recycled content (their EcoTouch insulation uses 65% recycled content, minimum 47% post-consumer recycled glass).

The lesson: If your moat depends on materials you don’t control, you need dual strategies—both securing existing supply chains AND developing alternative formulations.

USG/Knauf: The Gypsum Oligopoly’s Supply Chain Dance

USG (now owned by Knauf) and the gypsum wallboard industry provide another instructive case.

The industry is highly concentrated—a few large players with company-owned mines and coast-to-coast distribution. Geographic concentration is strategic: plants locate near raw materials because gypsum has a low value-to-weight ratio (it’s expensive to ship).

USG’s Plaster City facility in California operates the last industrial narrow-gauge railway in the United States—a 26-mile line hauling gypsum from their quarry. That’s a serious moat. The estimated deposit contains 25 million tons.

But here’s the vulnerability: 93% of U.S. gypsum wallboard imports come from just two countries—Mexico (96% of those imports) and Canada.

When the Russia-Ukraine war disrupted supply chains in 2022, Mexican gypsum prices jumped 12% in a month. Indian cement companies saw logistics costs rise 4% annually while raw materials like fly ash and gypsum surged 7% year-over-year.

Natural gypsum production dropped 1% YoY in Q1 2025. Lead times for steel (often bundled with wallboard in construction orders) hit 12 weeks—five times normal.

Eagle Materials, which owns nearly all its raw materials, raised wallboard prices 33% YoY and kept raising them. Companies without vertically integrated supply chains got squeezed.

The cautionary principle: Owning your supply chain is a moat. Depending on a supply chain you don’t own is a noose.

The Counter-Example: Owens Corning’s Manufacturing Excellence

Owens Corning (the Pink Panther insulation company) demonstrates how to build moats through operational excellence rather than raw material control.

Their competitive advantages:

- Brand Recognition: The Pink Panther trademark (OC was the first company to trademark a color in 1986)

- Manufacturing Scale: 31 insulation facilities, 30 composites facilities, 16 roofing facilities across 31 countries

- Recycled Content Strategy: Uses locally sourced recycled glass (partnering with Ripple Glass in Kansas City to reduce landfill waste)

- Diversification: Three business segments (Composites, Insulation, Roofing) reduce exposure to any single market downturn

But here’s what separates them: Owens Corning recognized that in commodity-adjacent markets, your moat is your manufacturing efficiency and customer relationships—not your raw materials.

When the housing market crashed in 2009, they didn’t just hunker down. They fundamentally shifted their strategy to measure and create customer value—interviewing 120+ customers in six weeks and achieving 600% ROI in the first year.

They discovered their “investments” weren’t actually helping customers differentiate. They’d become a transactional supplier despite thinking they had strong relationships.

The insight: In highly competitive, somewhat commoditized markets, your true moat is whether customers make more money with you than with alternatives.

Not brand. Not scale. Not even product quality. Value creation.

The Moat-Building Framework for Building Products

So how do you build defensible advantages without building a trap?

1. Know What You’re Actually Defending

Product managers should use this structured approach:

Step 1: Brainstorm key competitors and analyze what differentiates your product

Step 2: Synthesize differences into strategic themes

Step 3: Determine which can be developed into sustainable competitive advantages

Step 4: Stress-test each advantage: “If a competitor copied this, how long would it take and what would it cost them?”

If the answer is “a few sprints,” it’s not a moat.

Real moats are built in operations, customer experience, and ecosystem integration.

2. Distinguish Between Protective Moats and Dependency Traps

Protective Moats:

- Manufacturing scale you can flex up or down

- Brand reputation earned through consistent quality

- Regulatory approvals that reflect genuine safety/performance

- Customer relationships based on value creation

- Patent portfolios that support rather than replace innovation

Dependency Traps:

- Single-source raw materials you don’t control

- Proprietary formulations with no backup suppliers

- Customer lock-in through data hostage-taking

- Regulatory capture that makes you complacent

- Distribution exclusivity that prevents market evolution

3. Apply the Profit Arc™ Principles

Every moat decision should pass through these filters:

Design for Manufacturability: Can you actually produce this at scale? What happens when your supplier raises prices 30%?

Supply Chain Resilience: Do you have alternative suppliers? Alternative materials? Can you make this profitably if your primary input doubles in cost?

Market Validation: Are customers willing to pay for this advantage? Or are they actively looking for ways around it? Do you have to sacrifice significant margin to get adoption?

Portfolio Optimization: Does this moat make your entire portfolio more defensible, or just one SKU?

True North Alignment: Does this advance your mission, or just create artificial barriers?

4. Build Bridges, Not Walls

The companies who will thrive in the next construction cycle are those who understand this.

The Vertical Integration Question

Given the insanity in supply chain of the past 3-5 years, you may have wondered more than once if you should vertically integrate.

Vertical integration largely depends on your Profit Arc.

Vertical integration makes sense when:

- Your raw material has volatile pricing and limited suppliers (like Eagle Materials owning gypsum deposits)

- The acquisition genuinely reduces costs or improves quality (like Builders FirstSource buying truss plants)

- You’re protecting against a realistic existential threat (like Home Depot acquiring SRS Distribution to secure contractor relationships)

Vertical integration is a trap when:

- You’re doing it defensively because you’re scared, not strategically because it improves value

- The acquisition distracts from core competencies (do you really want to be in the mining business?)

- You’re creating fixed costs in a variable-cost world

- You’re trying to solve a relationship problem with an ownership solution

The James Hardie approach is instructive: They don’t own their entire supply chain. But they maintain deep supplier relationships, invest in alternative materials research, and build operational flexibility through their operating system.

They’re resilient through capability, not control.

The Future-Proof Strategy: Moats That Adapt

Whether your moat is a proprietary software platform or a proprietary fastening system, the same logic applies: lock-in without value creation is a countdown timer. Bundled pricing without modular options is an invitation for a focused competitor. Supply chain control without supply chain alternatives is a single point of failure. The moats that hold are the ones that make the ecosystem stronger, not the ones that extract from it.

The companies that will dominate building products and contech in the next decade aren’t the ones with the deepest moats.

They’re the ones with the most adaptive moats—competitive advantages that evolve with market conditions rather than ossify against them.

James Hardie’s 90% market share is defensible because they keep investing in new formulations, new capacity, and new markets. Not because they make it impossible to compete.

Autodesk’s design software dominance is sustainable because they’re building bridges to new workflows rather than forcing everything through their tools.

Owens Corning’s Pink Panther brand endures because they measure customer value religiously and adapt their offerings accordingly.

The companies getting disrupted? They’re the ones who built fortresses and then fell asleep inside them.

The Bottom Line

If your competitive advantage can be eliminated by:

- A supplier raising prices 30%

- A customer switching to a competitor out of frustration rather than performance

- A new entrant offering “good enough” at 50% of your price

- A regulatory change you didn’t see coming

…then you don’t have a moat. You have a dependency wearing a disguise.

Real moats in building products and contech come from:

- Manufacturing excellence that delivers consistent quality at competitive cost—regardless of input price fluctuations

- Customer value creation that’s measurable, demonstrable, and aligned with their actual needs—not your assumptions about their needs

- Supply chain resilience through multiple sources, alternative materials, and operational flexibility—not control for control’s sake

- Continuous innovation that makes your competitive advantages dynamic rather than static

- Ecosystem integration that creates value for everyone in the chain—not just extracts it

The Profit Arc framework demands that we design profitability into every product from day one. That includes designing sustainable competitive advantages — ones that protect you without imprisoning you.

Because in construction, the only thing worse than having no moat is having a moat that becomes your drowning pool.

Your Turn: The Moat Audit

Ask yourself these questions about your product portfolio:

The Dependency Test:

- If my top supplier doubled their prices tomorrow, could I still make this product profitably?

- Do I have at least two viable sources for every critical input?

- Can I reformulate with alternative materials if needed?

The Customer Value Test:

- Do customers buy from me because I create measurable value, or because switching is too painful?

- Would my customers recommend me to a competitor’s customer?

- If I raised prices 20% tomorrow, would customers pay it gladly or start shopping?

The Innovation Test:

- When was the last time I meaningfully improved this product’s value proposition?

- Am I investing in moat maintenance, or just counting on what I built years ago?

- If I were starting from scratch today, would I design this product the same way?

The Ecosystem Test:

- Do my competitive advantages make the entire value chain stronger, or just transfer margin to me?

- Am I a partner my customers want to grow with, or a supplier they’re stuck with?

- When I win, do my distributors, contractors, and end users win too?

If you don’t like your answers, you don’t have a moat problem.

You have a strategy problem masquerading as a competitive advantage.

The good news: you can fix it. But only if you can name it.

Which of these moats is quietly becoming a liability in your own portfolio?

Drop it in the comments or send me a DM spectoscale.com.